The Core Components of Comprehensive Financial Planning

Many of us wish for a future filled with financial stability and success. But turning that wish into reality needs a clear plan. Financial planning is our strategic guide. It helps us manage our money today to reach our goals tomorrow. This includes everything from saving for a home to a comfortable retirement.

In this extensive guide, we will explore financial planning. We will define what it is and why it is so important. We will break down its core parts and show you how to build your own plan, step-by-step. Understanding your financial health starts with clear records. Effective Bookkeeping and financial planning are the bedrock for all future decisions.

We will also look at the role of professional advice and how to adjust your plan as life changes. Our aim is to give you the tools and knowledge for long-term financial success in April 2026 and beyond.

At its heart, financial planning is about making the best use of your money to achieve your life’s ambitions. It’s a dynamic process, not a one-time event, encompassing various aspects of your financial life. A comprehensive financial plan acts as a strategic roadmap, detailing your current financial situation, your future goals, and the strategies required to bridge the gap between the two.

The core components typically include:

- Net Worth Calculation: This is your financial snapshot at a given moment. It’s derived by subtracting your total liabilities (what you owe) from your total assets (what you own). Assets can include cash, investments, real estate, and other valuables. Liabilities cover mortgages, loans, credit card debt, and other obligations. Understanding your net worth provides a baseline for measuring financial progress.

- Cash Flow Analysis and Budgeting: This involves meticulously tracking your income and expenses to understand where your money comes from and where it goes. Positive cash flow is the lifeblood of financial health, allowing for savings and investments.

- Emergency Funds: A crucial buffer against life’s unexpected events, typically covering three to six months of essential living expenses.

- Debt Management and Reduction: Strategically addressing and reducing high-interest debt frees up cash flow for other financial goals.

- Insurance and Risk Management: Protecting your assets and income from unforeseen circumstances like illness, disability, or property damage.

- Investment Planning: Aligning your investments with your risk tolerance and long-term goals, whether for retirement, education, or other significant purchases.

- Retirement Planning: A long-term strategy to ensure financial independence in your later years.

- Tax Planning: Proactively managing your finances to minimize tax liabilities and maximize after-tax returns.

- Estate Planning: Ensuring your assets are distributed according to your wishes and that your loved ones are cared for.

These elements are interconnected, and a change in one often impacts others. For instance, reducing debt can free up funds for an emergency fund or investments, while smart tax planning can accelerate wealth accumulation.

Establishing a Foundation with Cash Flow and Budgeting

The journey toward financial stability begins with a clear understanding of your cash flow. This means diligently tracking every dollar that enters and leaves your accounts. Income tracking involves understanding all sources of revenue, while expense management requires categorizing and monitoring your spending habits. The goal is to achieve positive cash flow, where your income consistently exceeds your expenses.

Budgeting is the tool that facilitates this. While various methods exist, one popular guideline is the 60/30/10+15 rule (or similar variations). This might suggest allocating a certain percentage of income to essential expenses, discretionary spending, debt repayment, and savings/investments. The key is to find a system that works for you, promotes financial discipline, and allows for automated savings. By automating transfers to savings and investment accounts, you “pay yourself first,” making consistent progress towards your goals. This foundational step is often where individuals gain the most immediate control over their financial future, identifying areas for adjustment and freeing up resources for higher priorities.

Risk Management and Insurance Integration

An often-overlooked, yet critical, component of financial planning is robust risk management and insurance integration. Life is unpredictable, and without adequate protection, a single unforeseen event can derail years of careful financial planning. Our approach emphasizes safeguarding your financial health through appropriate insurance coverage.

This includes securing comprehensive health insurance to cover medical emergencies and ongoing care, especially considering that a 65-year-old individual who retired in 2025 may need $172,500 in after-tax savings to cover health care expenses in retirement, on average. Disability coverage is equally vital, replacing a portion of your income if you’re unable to work due to illness or injury. Liability protection, often integrated into home or auto insurance, shields your assets from legal claims. Property insurance (homeowners, renters, or auto) protects your physical possessions. Strategic risk mitigation involves identifying potential financial threats and implementing measures to minimize their impact, ensuring long-term stability for you and your family. This proactive stance provides peace of mind, knowing that your financial plan is resilient against unexpected challenges.

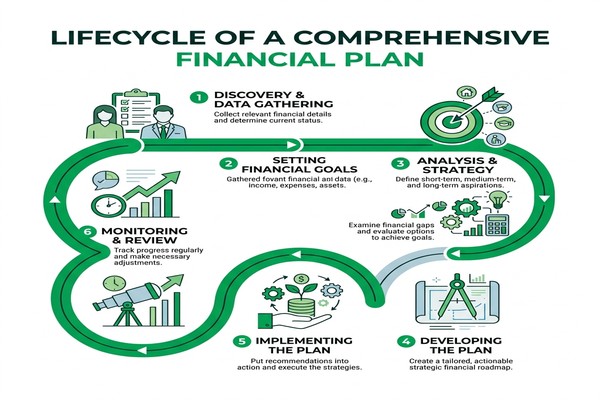

Building Your Roadmap: A Step-by-Step Guide

Creating a financial plan can seem daunting, but by breaking it down into manageable steps, we can build a clear and actionable roadmap to your financial future. This process is highly personalized, reflecting your unique circumstances, aspirations, and risk tolerance.

- Define Your Goals: The first and most crucial step is to clearly articulate your financial objectives. These can be short-term (e.g., saving for a down payment on a house in three years) or long-term (e.g., retirement at age 65, funding a child’s education). Specific, measurable, achievable, relevant, and time-bound (SMART) goals provide direction. For example, instead of “save for retirement,” aim for “save $1 million by age 65.”

- Assess Your Current Financial Situation: This involves calculating your net worth and conducting a thorough cash flow analysis. Gather all relevant financial documents: bank statements, investment accounts, loan details, credit card statements, and pay stubs. This provides a realistic starting point.

- Develop Your Plan: Based on your goals and current situation, begin crafting strategies. This includes setting a budget, determining how much you can realistically save and invest, and outlining a debt repayment strategy. This is where you leverage insights from Intelligent financial planning tools and resources to model various scenarios and optimize your path forward.

- Implement Your Plan: This is where action happens. Open necessary accounts (e.g., investment accounts, dedicated savings accounts), set up automated transfers, and start putting your debt reduction strategy into practice. Consistency is key here.

- Monitor and Adjust: A financial plan is a living document. It needs periodic review and adjustment. Life events, market changes, and evolving goals will necessitate updates. We recommend at least an annual review, but more frequent checks might be needed during periods of significant change.

Integrating Investment and Retirement Strategies in Financial Planning

Investing is a cornerstone of wealth accumulation, particularly for long-term goals like retirement. Our approach emphasizes aligning your investment strategy with your personal risk tolerance. Understanding how much risk you’re comfortable taking is paramount, as it dictates your asset allocation – the mix of stocks, bonds, and other investments in your portfolio.

For retirement, maximizing contributions to tax-advantaged accounts is a key strategy. In April 2026, the maximum 401(k) contribution is $24,500, with those age 50 and above able to contribute up to $32,500 (or $35,750 for ages 60-63 if allowed by their plan). Similarly, IRA contributions have limits, often with additional catch-up contributions for those 50 and older. We also emphasize the power of compound interest, where your earnings generate further earnings, significantly accelerating wealth growth over time. Diversification across different asset classes and geographies helps mitigate risk, while regular portfolio rebalancing ensures your investment mix remains aligned with your goals and risk profile. Furthermore, Health Savings Accounts (HSAs) offer a triple tax advantage (tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses) and can serve as an excellent supplemental retirement savings vehicle, especially for healthcare costs in retirement.

Tax Efficiency and Strategic Optimization

Effective tax planning is not just about filing your annual return; it’s an ongoing, proactive strategy integrated into your overall financial plan. Our goal is to help you minimize your tax liability legally, maximizing the money you keep and can reinvest. This involves leveraging various tax-advantaged accounts, such as 401(k)s, IRAs, and HSAs, which offer benefits like tax-deductible contributions, tax-deferred growth, or tax-free withdrawals.

We also consider strategies like maximizing available deductions and credits, which can reduce your taxable income. For investors, understanding capital gains and the potential for loss harvesting can significantly impact your tax burden. Given that tax laws and brackets can change (we factor in the 2026 tax brackets), a proactive tax strategy involves continuous monitoring and adjustment. This ensures that every financial decision, from investment choices to major purchases, is made with its tax implications in mind, contributing to your long-term financial health.

Advanced Pillars: Estate Management and Wealth Transfer

Beyond accumulating wealth, a comprehensive financial plan addresses how that wealth will be managed and transferred according to your wishes. Estate planning is not just for the ultra-wealthy; it’s a vital component for anyone who wants to ensure their legacy and protect their loved ones. We understand that an estimated $30 trillion is expected to pass from baby boomers to their heirs over the coming decades, underscoring the importance of thoughtful planning.

Key elements include:

- Wills: Legally outlining how your assets will be distributed and who will care for minor children.

- Trusts: Providing more control over how and when assets are distributed, potentially offering tax benefits and avoiding probate.

- Beneficiary Designations: Ensuring that retirement accounts, life insurance policies, and other assets pass directly to your chosen beneficiaries, often bypassing probate.

- Guardianship: Designating guardians for minor children in your will.

- Powers of Attorney and Healthcare Directives: Appointing individuals to make financial and medical decisions on your behalf if you become incapacitated.

- Estate Taxes: Planning to minimize potential estate taxes, ensuring more of your wealth passes to your heirs.

Incorporating Life insurance financial planning can be a critical strategy within estate planning. Life insurance can provide liquidity to cover estate taxes, replace lost income, or create an inheritance for heirs, even if other assets are tied up. It’s a powerful tool to ensure your family’s financial security and the fulfillment of your legacy, irrespective of the size of your estate.

The Role of Professional Guidance in Financial Planning

While DIY financial planning is possible, especially with the abundance of free tools and resources available (like calculators from Investor.gov), the complexity of modern finance often benefits from professional guidance. The demand for personal financial advisors is expected to grow faster than average, at a rate of 13% through 2032, reflecting the increasing need for expert help.

When seeking professional advice, the choice between a DIY approach and hiring an advisor often comes down to the complexity of your financial situation, your time availability, and your comfort level with making intricate financial decisions. If you opt for an advisor, we strongly advocate for working with a fiduciary, fee-only advisor. A fiduciary is legally obligated to act in your best interests, putting your needs before their own. A fee-only structure means they are compensated directly by you, eliminating potential conflicts of interest that can arise from commissions on products they recommend. This model ensures unbiased advice, fostering trust and aligning the advisor’s success with your own. Certified Financial Planner (CFP®) professionals, for example, adhere to a strict code of ethics and possess comprehensive knowledge across all areas of financial planning. This professional partnership can significantly improve financial confidence, helping to reduce the stress associated with managing complex financial decisions.

When to Review and Adjust Your Strategy

A financial plan is not a static document; it’s a dynamic guide that must evolve with your life and the world around you. Regularly reviewing and adjusting your strategy is paramount to ensuring it remains relevant and effective.

We recommend at least an annual audit of your financial plan. This allows us to assess progress toward your goals, evaluate the performance of your investments, and make necessary tweaks. However, certain life events serve as critical triggers for immediate review:

- Significant Life Changes: Marriage, divorce, the birth or adoption of a child, or the death of a spouse or family member fundamentally alter your financial landscape and goals.

- Career Changes: A new job, promotion, job loss, or starting your own business will impact your income, benefits, and potentially your risk tolerance.

- Major Purchases or Sales: Buying a home, selling a business, or inheriting a substantial sum (a windfall) requires re-evaluation of your asset allocation and overall plan.

- Economic Shifts: Periods of high inflation, market volatility, or changes in interest rates (which are always a factor in 2026 economic trends) can impact your purchasing power, investment returns, and debt obligations.

- Regulatory Changes: Updates to tax laws, retirement account rules, or estate planning regulations necessitate adjustments to ensure your plan remains optimized.

For instance, if you get a new job with a higher salary, we’d review your budget, increase savings contributions, and potentially adjust your investment strategy. If you experience a significant market downturn, we’d assess if your risk tolerance has changed and if your portfolio still aligns with your long-term objectives. People with a financial plan are less likely to worry about whether they are on track to meet their financial goals (36% vs. 47% without a plan), highlighting the confidence that comes from a well-maintained strategy. Regular adjustments ensure your plan remains a living, breathing document that adapts to your journey, rather than a forgotten relic.

Frequently Asked Questions about Financial Planning

When should I review and update my financial plan?

We advise reviewing your financial plan at least once a year, typically at a consistent time each year, such as the start of the year or before tax season. However, certain trigger events necessitate immediate updates. These include significant income changes (promotion, job loss), family expansions (marriage, children), nearing retirement, or major regulatory shifts in tax laws or investment rules. Think of it as a living document that needs regular attention to stay aligned with your evolving life.

What are the primary benefits of having a formal financial plan?

The benefits of a formal financial plan are extensive. Firstly, it significantly reduces financial stress and improves overall financial confidence. With a plan, you gain clarity on your goals and a defined path to achieve them. It facilitates wealth accumulation by optimizing savings and investments, helps in effective debt elimination, and ensures the security of your legacy through proper estate planning. It provides peace of mind, knowing you’re making informed decisions for your future.

How do I choose between a DIY approach and a professional advisor?

The decision between managing your finances yourself or hiring a professional advisor depends on several factors. Consider the complexity of your financial situation; if you have multiple income streams, diverse investments, or significant tax considerations, a professional might be beneficial. Evaluate your time availability and willingness to dedicate hours to research and management. For those seeking specialized technical expertise, behavioral coaching, or assistance with complex financial products, a professional advisor, particularly one who adheres to a fiduciary standard and operates on a fee-only basis, can provide invaluable unbiased advice.

Conclusion

Embarking on the journey of financial planning is an empowering step toward securing your future. We’ve explored how a comprehensive financial plan acts as your strategic guide, helping you navigate the complexities of wealth management, from establishing a solid foundation with cash flow and budgeting to integrating sophisticated investment, tax, and estate planning strategies.

In April 2026, the landscape of personal finance continues to evolve, making adaptability and informed decision-making more crucial than ever. Whether you choose a DIY approach, leveraging free resources like Investor.gov, or opt for the unbiased expertise of a fiduciary, fee-only advisor, the core principles remain constant: define your goals, understand your current situation, implement a strategy, and consistently review and adjust.

The statistics underscore the tangible benefits: reduced stress, increased confidence, and a higher likelihood of achieving your long-term financial goals. By embracing financial planning as an ongoing process, you’re not just managing money; you’re building a resilient future, preserving your wealth, and ensuring strategic growth for years to come. Your path to financial independence and lasting success starts with a well-crafted plan.